In the penultimate class, we will review key terms that you should know for the final exam.

·

Percentage

Change Formula – be able to calculate what the change in price was when

given

an old and a new price

·

Percentage

Discount Formula – you get x% off – the new sale price is?

·

Percentage

Mark-up Formula – you want to make x% profit over the cost of an item –

how

much should you charge?

·

Future

value formula – how much will the value of a savings or retirement account be worth

if it grows at x% per year, over a 10, 20, 30, or 40-year period? Be able to write out the formula to solve –

extra credit for using Excel to find the exact answer (future value)

·

What is

depreciation? By how much per year does

the average car depreciate in value?

·

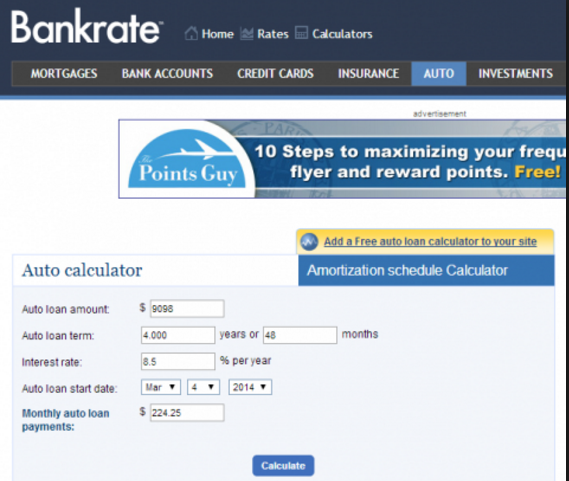

Be able

to use Bankrate.com to calculate the total interest paid on a car loan or a

mortgage

·

What web

sites would you go to for used car pricing information?

·

What is

net worth? How do you calculate it?

What is an asset? What is a

liability?

Give 3 examples of a

current liability.

·

What is a

budget? Surplus? Deficit? Is a budget

more related to net worth or net income?

Why?

·

What is

meant by the risk vs reward of an investment?

Which investments are risky?

Which investments are least risky?

Which investments give higher rates of return – risky ones or less risky

ones?

·

What is

the max percentage you should allocate to housing as far as your budget is

concerned?

·

What’s

the most you should pay for a house as a multiple of your annual gross income?

·

When

would you not consider buying a home?

Why?

·

What is

liquidity mean as far as investing is concerned? Which investments or assets are liquid? Which

are illiquid?

·

What are

the advantages of a Roth IRA and a 401K?

·

What are

the biggest expense categories (as a percentage of your gross income)?

·

Why are

many younger folks net worth negative while early retirees net worth positive?

·

List 3

good uses of credit (debt). List 3 bad

uses of credit (debt).

·

What is

the most important variable that the credit bureaus use in the calculation of

your FICO score?

·

Why

should you pay down your debt as fast as possible?

·

What is

an emergency fund? About how much should

you set aside for it in terms of number of total avg monthly expenses?

·

What is a

W-4 form? What are exemptions/allowances

on a W-4 used for? What other info is

required when filling out a W-4 form?

·

What is a

W-2 form? What key info do you find on

it?

·

What’s

the difference between APY and APR?

·

What is

the FICA tax? How much do employees

typically pay in to FICA as a percentage of their gross income?

·

Be able

to convert a decimal to a percentage to a fraction – esp for 1.0, 2.0, 0.5,

0.3333, 0.6666, 0.25, 0.2, 0.125, three-eighths, seven-eighths

·

What is a

credit vs a debit (in a checking account registry – transaction history)

·

How much

of a percentage gain do you need to get back to break-even after suffering a

loss of x%?

·

How to

factor in the cost of CT state sales tax into the final purchase price

·

What is

the historical rate of inflation in the U.S. and what does that do to the price

of an item over a 1-year, 2-year and 3-year period?

·

If you

double your money, what percentage increase is that? Same question for tripling your money.

If you have any questions, please ask. Good luck!